GLP-1 household spend reallocation: A cross-category demand guide for retail planners

Last Updated:

May 11, 2026

Reading time:

Time

mins

GLP-1 retail spend reallocation is the structural budget reorganization happening inside households that have adopted GLP-1 medication. Specific discretionary categories are being deliberately defunded. Specific health and maintenance categories are being actively prioritized. The substitution flow is visible in consumer conversation data before it confirms in transaction data.

TL;DR

What is GLP-1 retail spend reallocation? GLP-1 households exiting specific discretionary categories and entering specific health and maintenance categories simultaneously, reorganizing around health stability as the new budget priority.

What are the exit categories? Alcohol (partially physiological), takeout, impulse online purchases, and discretionary personal services.

What are the entry categories? Protein foods, hydration, produce, and GI management products.

What makes the alcohol signal different? A significant portion is physiological rather than discretionary and will not respond to any promotional intervention.

What is the sequencing rule? Defensive health spending is funded first. Expressive discretionary spending is deferred, not eliminated.

The substitution mechanism

The reallocation follows a predictable structure confirmed by consumer language:

"I cut back on some things like nails, some streaming apps and not buying takeout to justify the big price tag."

"Even with the cost of the injections, I'm still saving money by not buying 6 bottles of wine per week and rarely buying anything online."

Exit categories:

Entry categories:

Exit categories carry low positive sentiment. Entry categories carry high positive sentiment. The directionality is confirmed by both volume and sentiment simultaneously.

Understanding what GLP-1 retail impact means for cross-category commercial planning establishes the broader framework this substitution flow operates within.

The alcohol demand decline: Two groups, two responses

The alcohol signal contains a distinction standard category management cannot make.

Voluntary reducers at high positive sentiment may respond to non-alcoholic alternatives and premium low-alcohol products.

Physiological sensitivity cases at low positive sentiment describe biological changes, not deliberate choices:

"I can no longer eat even slightly spicy foods or any alcohol without making myself sick."

Physiological demand loss does not respond to promotional intervention or price reduction. Treating it as voluntary reduction is where promotional budget is wasted and margin is eroded.

The savings reframe

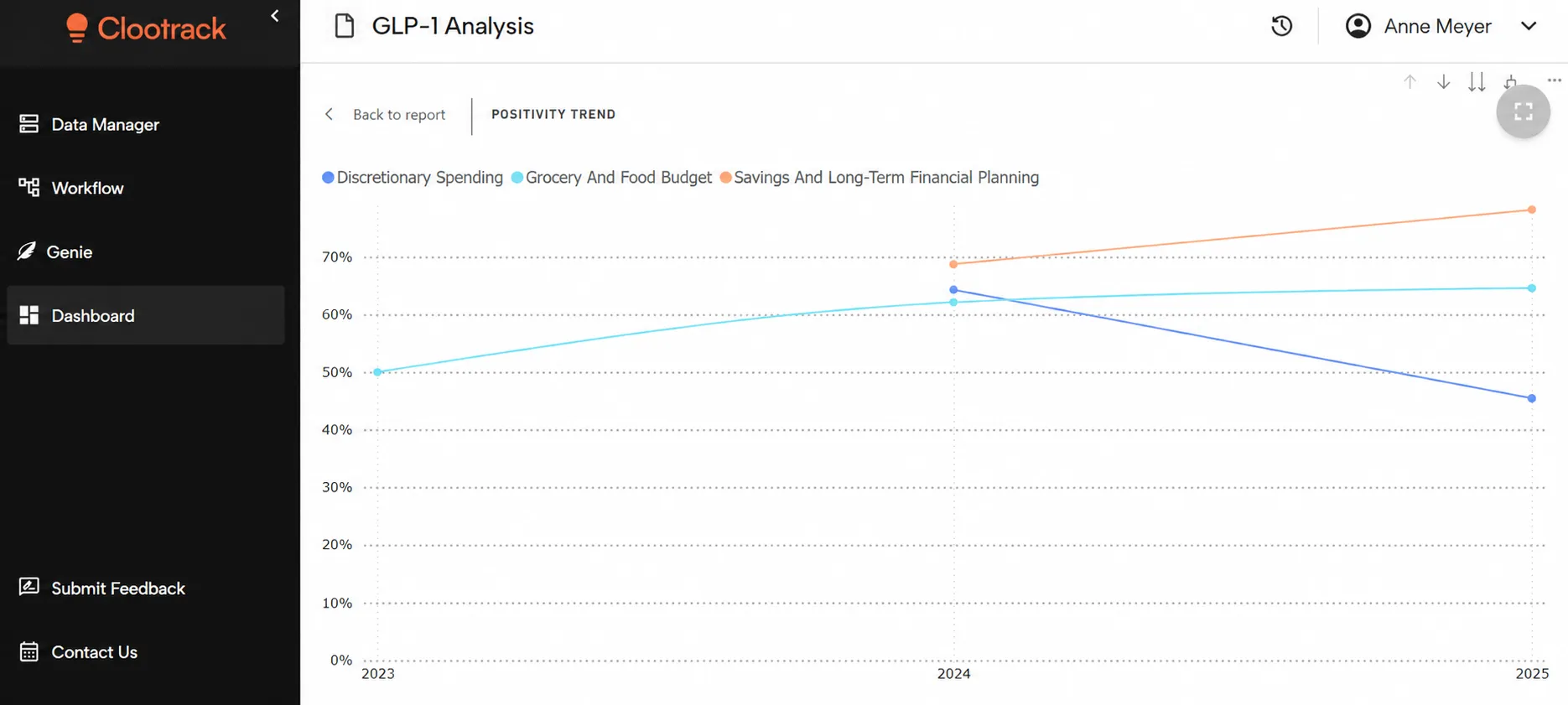

One signal in GLP-1 household spending has no equivalent in any other retail demand shift. Savings and Long-Term Financial Planning: 94 mentions, 76.6% positive sentiment, 349.4% MoM growth.

Consumers are not resigning to high medication costs. They are calculating downstream savings on food, alcohol, and impulse purchases that offset medication expense. A consumer who believes they are financially ahead is more likely to invest in adjacent health categories. This converts what appears to be budget pressure into a health investment motivation retailers can position against.

Defensive versus expressive spending sequencing

- Defensive spending (GI management, hydration, protein, firmness repair) is funded immediately. Biologically driven, recurring, promotion-independent.

- Expressive spending (fashion apparel, decorative cosmetics, indulgent grocery) is deferred, not eliminated. Recovery is linked to biological and psychological progress, not promotional triggers.

Presence during the hesitation period is the correct commercial posture. Promotional activation during the suppression window will not accelerate expressive category recovery.

For how beauty specifically reallocates within this sequencing see GLP-1 beauty category reallocation.

FAQs

What is GLP-1 retail spend reallocation?

The structural reorganization of GLP-1 household budgets around health stability, deliberately defunding discretionary categories and actively investing in health and maintenance categories following a defensive-first, expressive-later sequence.

Why is the alcohol demand decline in GLP-1 markets different from other category declines?

It contains two groups requiring different responses. Voluntary reducers may respond to non-alcoholic alternatives. Physiological sensitivity cases will not respond to any promotional intervention. Standard category management cannot distinguish between them.

What is the GLP-1 savings reframe?

GLP-1 consumers calculating medication costs are offset by savings on alcohol, takeout, and impulse purchases reframe their financial position as a net positive, making them more likely to invest in adjacent health categories.

How does GLP-1 affect grocery spending?

Grocery and Food Budget grew at 109.7% MoM at 64.1% positive sentiment. Protein Foods at 66.2% MoM and Produce at 86.6% MoM confirm health maintenance categories are prioritized before discretionary spending recovers.

What is the defensive versus expressive spending sequence?

Defensive health categories are funded immediately upon GLP-1 adoption. Expressive categories are deferred until weight stabilizes and identity confidence forms. The recovery timeline is biological, not promotional.

How can retailers detect GLP-1 spend reallocation before it confirms in sales data?

Through Financial Trade-offs conversation growth, sentiment asymmetry between exit and entry categories, and the Savings signal at 349.4% MoM growth, all appearing in consumer conversations before stabilizing into measurable category velocity changes.

Share :

Do you know what your customers really want?

Analyze customer reviews and automate market research with the fastest AI-powered customer intelligence tool.