VoC Analysis Report

The GLP-1 wallet reorganization

GLP-1 households are not spending less. They are redirecting spend with precision, and the retailers reading the exits as demand weakness are solving the wrong problem.

Cross-category substitution flow intelligence

This analysis maps household spending substitution across 95,854 GLP-1 consumer conversations using unsupervised AI thematic detection. Not category-level sales averages but actual budget reorganization tracking revealing the full directional substitution flow across GLP-1 influenced households.

2,776

Alcohol intake mentions

4 Years

Analysis window

U.S.

Market

Executive summary

GLP-1 household spending is not contracting. It is reorganizing around a new priority anchor: health stability. Specific discretionary categories are being deliberately defunded (alcohol, takeout, impulse online purchases) to offset medication costs and fund adjacent health behaviors. The substitution flow is identifiable and directional.

The alcohol signal is the most commercially significant shift in the dataset. A meaningful portion of the demand reduction is physiological rather than discretionary. GLP-1 users describe changed tolerance and sensitivity as biological effects, not deliberate choices. Physiological demand loss does not respond to promotional intervention, which distinguishes it from voluntary reducers who may respond to non-alcoholic alternatives.

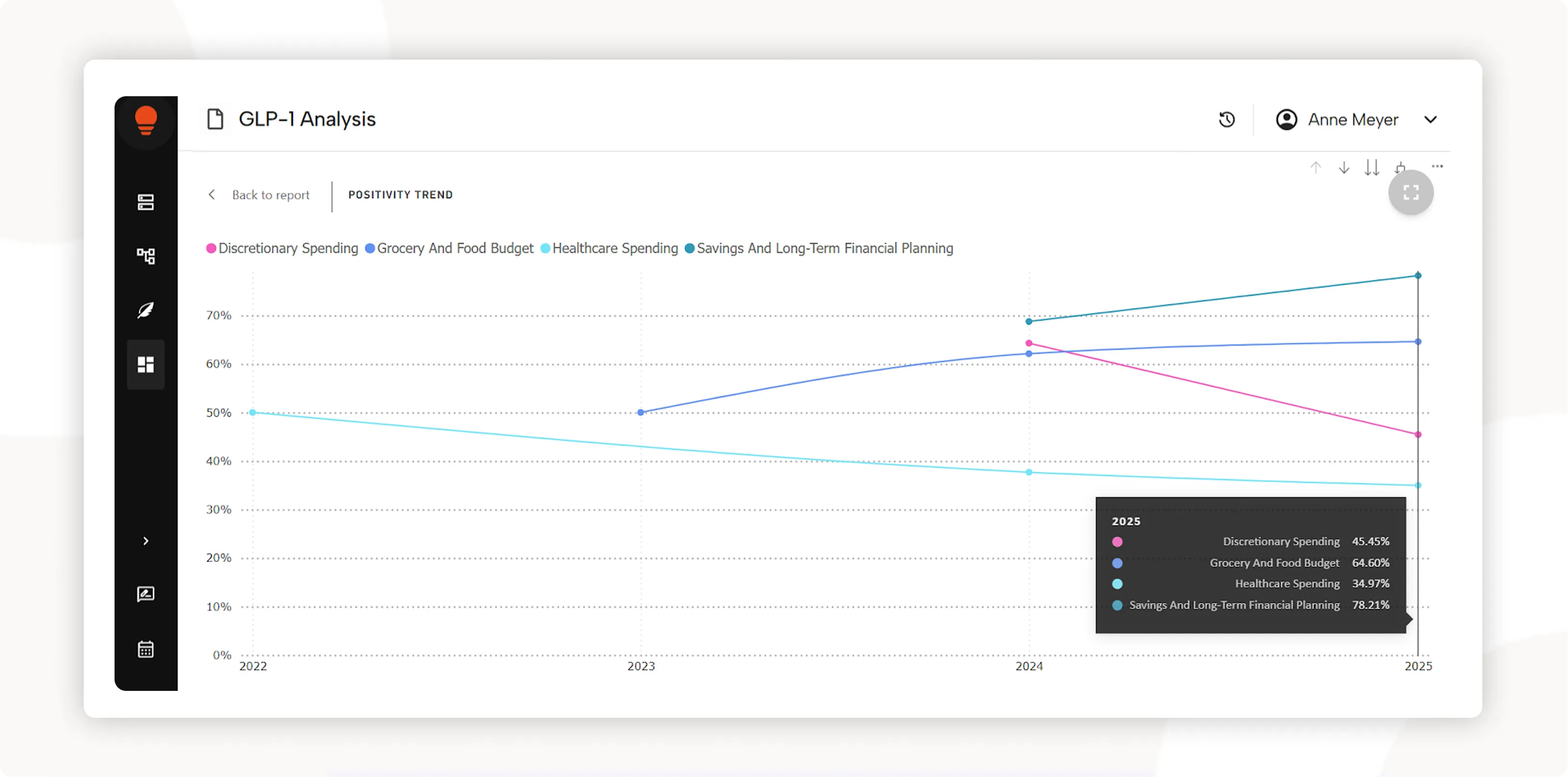

Savings and Grocery rising while Discretionary declines, the spend reallocation made visible across a four-year positivity trajectory.

Defensive health categories are funded first. Expressive discretionary categories are deferred, not eliminated. The sequence matters as much as the direction. The full substitution map showing where spend is exiting, where it is landing, and in what order is in the report.

Key findings

1

The alcohol demand shift is partially physiological, promotions will not recover it.

Alcohol Tolerance at 331.7% MoM growth at 32.5% positive sentiment and Sensitivity at 291.8% MoM at 14.4% positive describe biological changes, not preference shifts. Standard promotional intervention addresses the wrong mechanism.

2

GLP-1 households are reframing medication costs as a net financial positive.

Savings and Long-Term Financial Planning at 349.4% MoM growth at 76.6% positive sentiment confirms GLP-1 households are reframing their financial position positively. Health investment is being treated as reorganization, not a cost burden.

3

The exit categories are specific and deliberate.

Financial Trade-offs and Sacrifices at 92.3% MoM growth at 34.7% positive sentiment confirms the substitution logic is explicit in consumer language. This is structured budget reorganization, not generalized frugality.

4

Defensive spending is funded first. Expressive spending recovers later.

Grocery and Food Budget at 109.7% MoM growth at 64.1% positive sentiment and Protein Foods at 66.2% MoM growth confirm health maintenance categories are being actively prioritized. The sequence determines which retailers capture reallocation spend first.

Download Report

See the full substitution map before it confirms in your sales data.

The full GLP-1 spend reallocation analysis is in the report.

Insights report for CX, Ecommerce, Merchandising & Consumer Insights Leaders