VoC Analysis Report

The GLP-1 beauty repair economy

GLP-1 weight loss has shifted beauty spending from celebration to damage control. Most retail shelves are still organized around the motivation that moved on.

Sentiment-driven category reallocation tracking

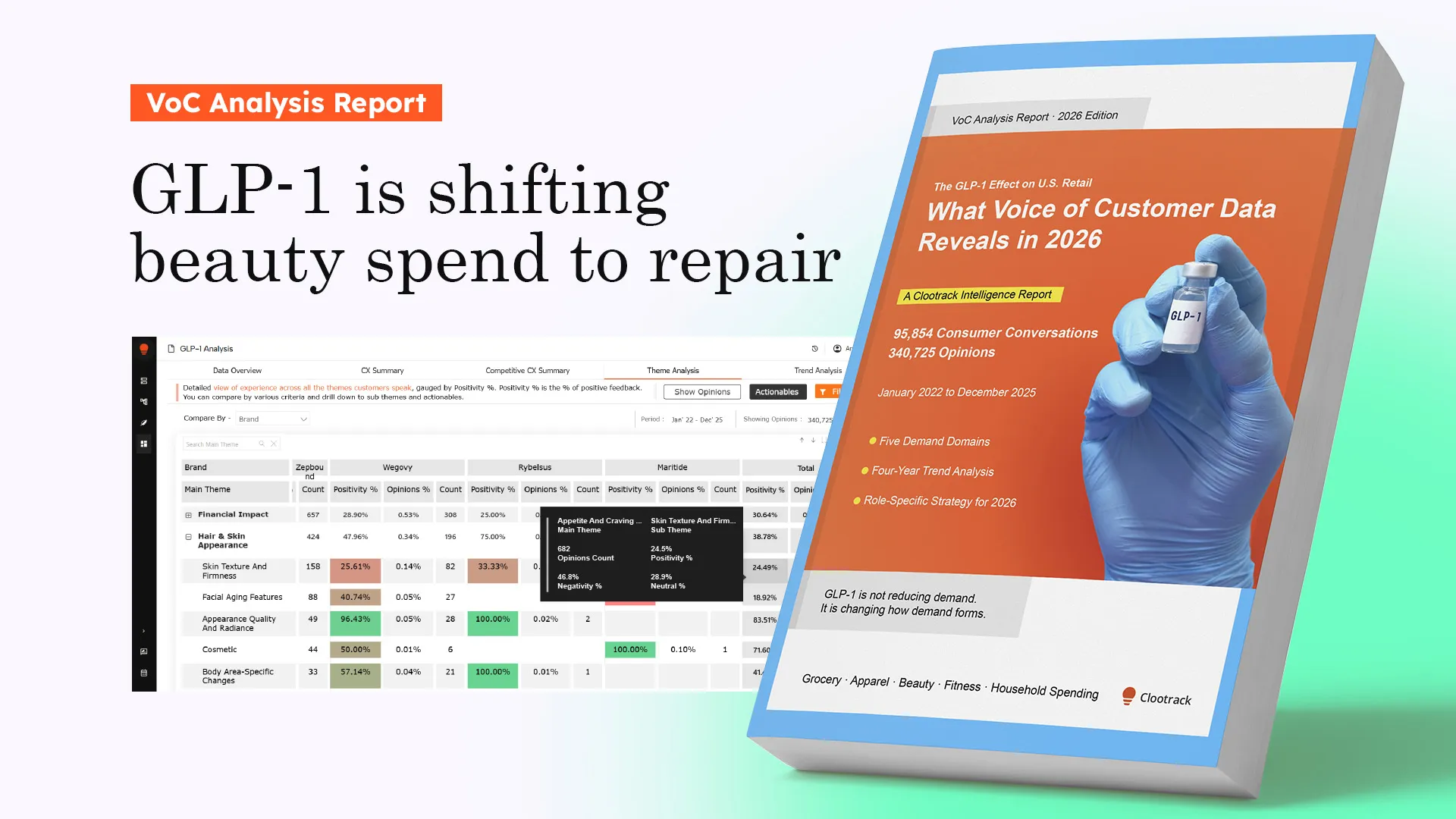

This analysis tracks beauty category reallocation across 95,854 GLP-1 consumer conversations using unsupervised AI thematic detection. Not beauty category growth averages but actual sentiment and motivation analysis revealing why the fastest-growing signal in the dataset is being commercially misread.

927.8%

MoM cosmetic intervention conversation growth

4 Years

Analysis window

U.S.

Market

Executive summary

GLP-1 weight loss produces facial volume changes alongside body composition changes. Hollowing under the eyes, skin laxity, increased visibility of fine lines, and accelerated visible aging are consistent themes in consumer narratives. The commercial response is not to stop losing weight. It is to seek corrective solutions.

Beauty spending is shifting from aspiration and decoration toward structural skin repair. Consumers are independently assembling multi-product corrective routines spanning firming serums, collagen supplements, red light therapy devices, and neck-specific treatments. No retailer is merchandising them that way. The economic unit has shifted from a single hero product to a structural skin management system.

Deflation anxiety and solution-seeking coexisting within the same consumer conversation set, the signal that retail beauty dashboards cannot currently surface.

A second behavioral layer adds complexity. Consumers are uncertain whether facial deflation is permanent before investing in solutions. This permanence hesitation creates a gap between intent and purchase that does not appear in any sales metric. The full mechanism and what retailers can do about it is in the report.

Key findings

1

The fastest-growing beauty signal is driven by damage control, not celebration.

Cosmetic Interventions at 927.8% MoM growth at 71.6% positive sentiment is not a beauty boom. It is a repair economy forming around facial deflation anxiety. Beauty shelves organized around aspiration are serving a motivation this consumer has moved past.

2

Ozempic face is a widespread concern with almost no positive sentiment.

At 15% positive sentiment and 140.3% MoM growth, facial deflation anxiety is accelerating and unresolved for the vast majority of consumers experiencing it. Low positivity at rapidly growing volume is the formation signal.

3

Consumers are building corrective routines without any retailer merchandising them that way.

The repair system spans firming serums, collagen supplements, red light devices, and neck treatments currently sitting in separate aisles. The consumer who has independently assembled this routine is not waiting for retail to catch up.

4

Appearance positivity dropped by approximately 42% in two years.

The decline from above 85% in 2022 to 43% by 2024 is the structural context behind every beauty category metric in this period. The partial recovery to 51% by late 2025 reflects the repair economy forming, not aspiration returning.

Download Report

See how beauty demand has reorganized and where it is heading.

The full GLP-1 beauty category analysis is in the report.

Insights report for CX, Ecommerce, Merchandising & Consumer Insights Leaders